Getting money is supposed to be the hard part, right. I mean, pulling a bank job takes hard work (and just working hard in general, I suppose, is no cake walk). So why does it have to be so complicated once you have it? (If you are seeking an answer to that question, please redirect your attention to the heavens and take a moment to raise your fist to the sky and rail at the universe; if you are seeking instead to try to understand what those complications are, read on.)

Inflation

Inflation is sort of like fat: you need some healthy fats in your diet to function, but if you have too much you’re in trouble. Rising prices are useful for a number of reasons. First of all, wages are sticky downwards. If a company needs to lower wages, they can do so by raising wage less than the rate of inflation, without lowering the nominal wage. Inflation also keeps the market moving: sitting with a huge pile of money under your mattress is less attractive when the money is losing value, and you would rather buy things now than when the price spikes. Bank or bond interest rates are also less attractive because high rates of inflation make real interest rates lower, which means less saving through those means as well.

Inflation also has a twin, deflation, which can have significantly worse consequences. If people think money is going to grow in value, they will put off spending it as long as possible. Think about if every single thing in the economy was always one day away from a clearance sale (yes, it is the things we love that have the power to hurt us most). You would never buy anything. And if no one is buying, then companies need to lay people off because they are not making money. And if people are unemployed and everything is about to go on clearance, you had better believe that they will be spending even less to try to make a finite supply last as long as possible. Meanwhile, companies won’t invest, because they won’t want to borrow, and without investment the cycle will just get worse. So, even without the positive effects, inflation is at least a way to stave off deflation.

That being said, we can have too much of a good thing (again, like clearance sales). One major issue is when inflation is felt unevenly throughout the economy. For instance, federal minimum wage has not changed in 11 years. The inflation chart from the bureau of labor statistics gives the inflation for the past 10; essentially, that means that the real minimum wage has decreased. Additionally, inflation rates are something that we calculate based on observable changes in the market, and our calculation system is by no means perfectly all encompassing. If price changes don’t affect every industry evenly, then people in certain industries are facing the same nominal income—that is to say, a lower real income, while others are getting that same real income (i.e. a higher nominal income, because of higher nominal sales, adjusted by the higher nominal cost of purchases). In the same vein, incomes are also redistributed from wage earners to profit earners, causing slower rise in wages.

Capital Gains Taxes

Capital Gains are taxed nominally, so inflation can lead to a decrease in real after tax income. Using a nominal measuring system, the IRS implicitly assumes that any price change on an asset reflects a change in the real value. Sometimes, it does (at least in part); often, it doesn’t. Resistance to higher rates of inflation largely stems from the fact that even if the inflation is controlled and expected, capital owners have to pay higher taxes without any change to their real wealth. If capital gains taxes were leveled against inflation adjusted value, then the tax would only be levied on the actual increase.

Neither a saver nor a lender be

The other major consequence of inflation has as much to do with inflation expectations as with inflation itself. Unexpected inflation makes saving and lending bad decisions, but it makes borrowing a great decision. If the money is losing value as you hold it, then you want to spend it as quickly as possible; if you are lending money and the real value you get back is not worth as much as the money you initially lent out, then you lose. Borrowing, on the other hand, is great if inflation goes up. It’s like borrowing a hundred dollars and paying back fifty instead of a hundred and fifty. Why does this have as much to do with expectations as with actual inflation? If we have a good sense of what the inflation rate is going to be, bonds, savings accounts, and other secure methods of saving will have interest rates that reflect that; lenders can additionally set interest rates to reflect that. Without certainty, lenders need to have interest rates that cover not just adjusting for inflation, but adjusting for the risks of a potentially high inflation rate. Borrowers, in turn, need to be protected from a sharp drop in inflation rate and will demand a lower rate of interest in accordance with their expectations. Income will be unexpectedly redistributed between borrowers and lenders if inflation differs from projections. Moreover, uncertainty will make reaching agreements significantly more complicated. Transaction costs and inefficiencies are often assumed to be nonexistent in economic models and theories, but imperfect information (another factor often assumed away) exacerbates them.

Vicious Cycles

Inflation also begets inflation, a phenomenon colloquially referred to as “letting the inflation genie out of the bottle.” Think less Robin Williams’ genie and more Jafar after he demands supreme cosmic power. If people start to worry about inflation, they start to spend rather than save, which means the demand for money goes up, which means inflation goes up which means people worry more about their money losing value and, well, you get the idea.

The Worst of the Worst

If the inflation genie runs totally rampant, it will cause hyper-inflation, the consequences of which are dire (which is probably why Disney movies just deal with magic genies and not inflation ones). There is some debate among economists over how hyperinflation is defined: quantitatively or qualitatively. The quantitative definition is that any country experiencing a 50% or higher monthly rate of inflation is hyperinflationary; the qualitative definition is a government that can no longer finance its expenses through taxes or borrowing and is forced to print money to finance day to day expenses. Either way, hyperinflation is cataclysmic to an economy, and is currently plaguing Venezuela. Headlines feature words like “nightmare,” “ravaged,” and “race for survival,” with one even titled “How hyperinflation stole Christmas in Venuezuela.” Noah Smith writes for Bloomberg, “Moderate inflation rates of 2 percent or even 15 percent are more of a nuisance than a scourge…But at 4,000 percent, inflation is like a hurricane. Savings are quickly wiped out. Expectations that saving will be fruitless deters people from investing, causing a recession and leading to capital flight. Nobody really knows how much their paycheck will be worth by the time they go to the store to spend it, so the entire labor system is thrown into chaos. Hyperinflation is probably one of a number of reasons why Venezuela, the country with the world’s largest oil reserves, now has starving children.” People’s wages no longer are able to cover basic living expenses, the price of a parking meter might change in the hour it takes to run errands, and prices are actually rising so quickly that people can barely even get their hands on the hard currency they need and are forced to wait in line at cash machines for small rations.

The plummeting value of the Bolivar compared to the dollar is only making matters worse; currency black markets are thwarting any attempt to stabilize the exchange rate, and the extreme price of foreign imports is slowing the economy by preventing imports of capital and equipment.

Venezuela’s latest policy attempt to deal with these issues was a major point of discussion for us last week, combining the cryptocurrency hot topic with a major economic issue and application. On January Fifth, Maduro announced the issuance “in coming days” of $ 5.9 billion in crypto-currency ‘Petro,’ where each petro is equal to one barrel of Venezuelan oil, fleshing out the details of the currency he initially announced with few specifications in December. Three weeks later, Maduro announced that a presale will be in hard currencies and other crypto-currencies, although it will not be available in the Bolivar. Another week later, the date of the presale was set for February 20th.

Critics are already outspoken: “Opposition politicians have already panned the project as a fanciful idea doomed to fail and useless at getting food to the millions who are suffering from product shortages and the world’s highest inflation,” one Reuters article writes, while another says, “Critics decry the petro as simply a way for the cash-strapped government to issue debt without being constricted by U.S. sanctions [which prohibit the purchase of newly issued Venezuelan debt].” Meanwhile, the US has already come forward to say that these Petros might indeed be in violation of the sanctions. CNBC also published the concerns of University of Oregon Professor Stephen McKeon, who wrote “Venezuela carries a lot of “counterparty risk” because it has little rule of law and falling oil production. If Venezuela fails to deliver the oil, he asks, what is the legal recourse for holders?”

While we’ve discussed the fundamental problem with crypto-currencies before, fundamental being the key word of course, the petro does address that issue and presents a potentially viable future avenue for crypto-currencies. Personally, I’m highly skeptical of the wisdom of pegging the value of currency to such a volatile asset. The EIA publishes data on Venezuelan oil prices; current prices are still $40 below their 2012 peak; the drop started small, but dropped as much as $43.78 in a single year since the decline began.

Meanwhile, one of our other econversations participants pointed out that Venezuela does not have the technological infrastructure to make a cryptocurrency anywhere close to universally accessible.

Though their methodology is unconventional, the principle of a total currency switch to help stabilize an out of control economy is not new. Brazil took what you might call the old fashioned approach to virtual currency; by virtual, I mean literally nonexistent. The entire nation of Brazil started listing their prices in a nonexistent currency called the URV or “unit of real value.” The exchange rate from the URV to cruzeiros fluctuated, but the URV price always stayed the same, giving the perception that prices had stabilized. Once the prices in URV were stable, the URV was converted into Brazil’s new currency: the real, still in use today, was born. Literally, Brazil made a fake currency, and then called it “the real” when they began to print it. I love economics.

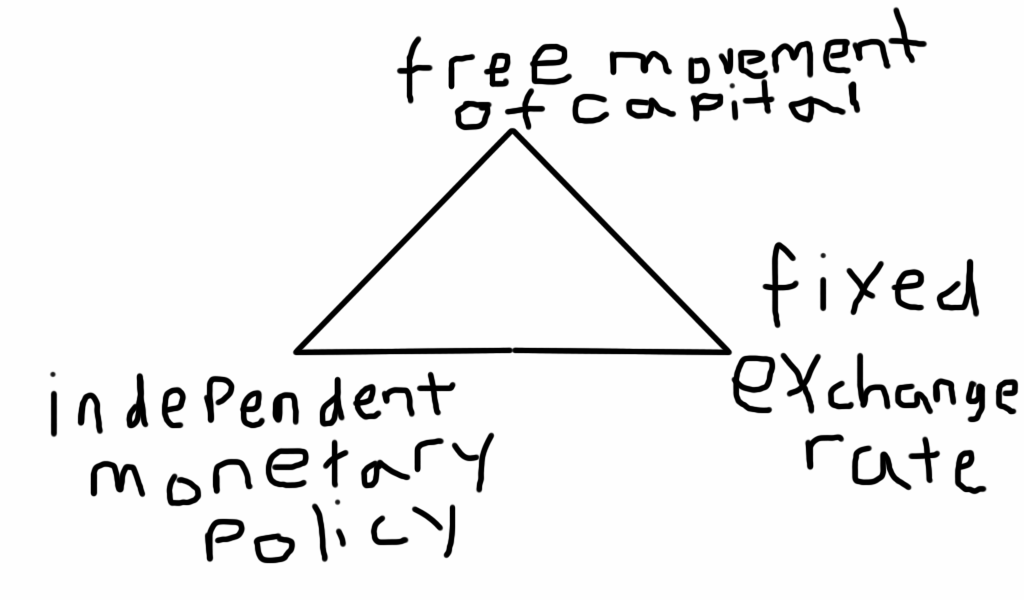

In 2000, Ecuador dollarized “after a financial crisis that saw its own former currency, the sucre, collapse so badly that people started putting their holdings into dollars, unofficially dollarizing the country’s economy. The government simply went ahead and made the switch official,” Eric Schnurer wrote for USA Today. Ecuador’s decision to dollarize is a perfect example of what is known as the trilemma or the impossible trinity. You’ve probably seen a diagram representing a trilemma before. They’re basically more bitter equivalents of the Panera you-pick-two menu.

The money trilemma looks like this:

So, why are these three things important?

Fixed exchange rates

Fixed exchange rates create stability, which is important both at home and abroad. If exchange rates are fluctuating wildly, the prices of imports and the income from exports are fluctuating wildly as well. Exchange rate changes are susceptible to some of the same concerns that apply to inflationary expectations as well, particularly because if the price (in local currency) of a capital import rises dramatically, the prices of the finished goods will follow suit. Fixed exchange rates also make a country more attractive to lenders who don’t want to wind up recouping less value than they loaned out (again, similarly to inflationary expectations with lenders).

Independent Monetary Policy

Put simply, national sovereignty is important, and if you cannot control your own economic policy in full, you are surrendering some of that sovereignty. When a specific government cannot tailor their own policy to their specific needs they are at best sacrificing a tool in their policy tool belt and at worst subjecting themselves to counterproductive policies imposed by the needs of other economies.

Free movement of capital

When capital moves freely, barring a market failure (which admittedly is by no means the de facto state of the global economy), the economy is able to function efficiently by allocating resources in the best ways. For a few examples, the European Commission goes into a little more detail on the explicit advantages.

Much like the facts of human physiology and the fact that you have 24 hours in a day, we just can’t change certain laws of economics. If you want a fixed exchange rate, then you can’t let the exchange rate be determined by the market, which means you have to control the inflow and outflow of your currency, and therefore restrict capital movements. Unless, of course, you use the same currency (the Euro; the US dollar), or manipulate the money supply to maintain the desired exchange rate. However, Ecuador’s monetary policy is now the United States’ monetary policy, regardless of whether or not Ecuador’s economy has the same needs as the US; nations in the Eurozone cannot unilaterally control their currency (and therefore monetary policy). Before Brexit, England had the benefits of the free movement of capital as a member of the EU, and controlled its own monetary policy because it could control the pound and the sterling, but the exchange rate between the two currencies fluctuated. Had Britain wanted a fixed exchange rate, they would have had to tailor their monetary policy to the Eurozone’s to keep the exchange rates constant.

In Venezuela, the Government is attempting to fix the USD/bolivar exchange rate at 10 bolivars per dollar, which means a heavy capital restriction. The actual market value of the USD is well over 100,000 Bolivars on the black market exchanges that have been running rampant.