Econversations will resume in Fall 2019 from September 25 onward. As usual, we will meet outside Davis Café in the Alvarez Student Union from 3:50pm to 4:50pm.

However, Econversations Blog will remain suspended until next academic year.

Shyam Gouri Suresh

Econversations will resume in Fall 2019 from September 25 onward. As usual, we will meet outside Davis Café in the Alvarez Student Union from 3:50pm to 4:50pm.

However, Econversations Blog will remain suspended until next academic year.

In 1957, Sergei Pavlovich Korolev was building ICBMs for the Soviet Union. He wasn’t a fervent communist, as Stalin had sent him to the Gulags in 1938, where he stayed until 1945.

Anyway, none of the ICBMs he built were functional. He was using liquid fuel, which was much more powerful but less stable. Liquid fuel rockets had to be filled with fuel immediately before launch because they were liable to explode randomly if left fueled. This is in contrast to solid fuel rockets, which are less powerful but can be launched on command, precisely what is needed for an ICBM. Luckily for the world, Sergei Pavlovich didn’t care about the Soviet ICBM program. He just wanted to explore space. So he built terrible ICBMs but made incredible technological breakthroughs. I am convinced he is why we’re alive, because Khruschev was a trigger happy lunatic. (3) Think of how much worse the Cuban Missile Crisis would have been if he actually had something to back it up. (1)

Anyway, after a rocket launch, Sergei Pavlovich begged Khruschev to let him shoot a radio into orbit. Khruschev said something along the lines of “but there are bigger problems on earth, what if the capitalist West take all the space benefits for themselves?” But Sergei Pavlovich kept bothering him, and since Khruschev didn’t care he finally said yes. That was sputnik.

I hate to paint with a broad brush, but every single space cynic in the world is myopic and a thief of joy. I don’t know what else to say, it’s not a difference in opinions or values, you are simply wrong. You are Khruschev, and I am someone fangirling outside Sergei Pavlovich’s dacha.

I’ll respond to a few of the most common attacks against space research/colonization.

1) There are still problems on Earth.

What an astute observation. However, at what point would you consider Earth post-problem enough to justify this scientific research? Because I would argue that from a caveman perspective, we are essentially post-scarcity and post-problem. But due to relativism, the goalposts keep changing, so this line of argument is intended to put space to bed permanently. But why single out space research specifically? Humans still have problems, so why spend money on PETA? GreenPeace? There are still problems in the US, so why spend anything on foreign aid? Space research is just scientific research, which I imagine many liberal space cynics will be in favor of. Also, where do you think this money is being spent? It’s all on earth. Check out the next section for the space research benefit multiplier. All this research will have dual use applications back on earth. To survive in space, new medical, engineering, and AI research will need to be done, all of which will transform life here on earth.

2) What if there are no spillovers and the goods are all taken for rich people?

I’m going to use the example of genetically engineered super babies from our meeting. The typical product cycle is that goods are available early on for rich people exclusively because of high prices, but as the cost falls, it moves into a mass market. I don’t see why this is inherently evil. I also don’t see why this argument is reserved for space-related things. I would argue that microwaves and cars made a bigger immediate impact than this (gene editing) will, but few (if any) people argued to restrict these goods because they were going to rich people first. Profit is just a marker of value. You heard it here first, the first trillionaire is going to be an asteroid miner. Once this is done, earth destroying resource extraction will be done less and less until it disappears entirely. Manufacturing can also be exported past earth’s orbit.

A 1992 report by a research journal named Nature found that NASA expenditures had a regional effect multiplier from direct and indirect sources of up to 8. The header of the paper reads “The economic benefits of NASA’s programs are greater than generally realized. The main beneficiaries (the American public) may not even realize the source of their good fortune.” NASA has transitioned away from being a direct research organization to what that provides resources and forms partnerships with businesses and outside research groups. A compelling case could be made that this will increase that multiplier.

(2)

“But Jake, what if the private companies take their proprietary technology for themselves? That’s not what NASA did!” True, but that is the case for all private R&D, which is not really what this is. There is a complex ecosystem required in space. Any company that figures out how to do something profitable in space will require a great number of inputs to operate successfully. Even Lockheed Martin, Boeing, and the like have to subcontract out to finish their rockets… even though their job is literally to build rockets. Then you add in habitation facilities, communications, life support, etc. into the mix, and you can imagine how widely the benefits would flow. The only way to profitably do space research is to have the end product have useful applications here on earth, which will entail selling it here.

3) Rich people will all leave earth and dominate space.

I saw Elysium too, but it’s off in a variety of ways. First, space is cold, dark, inhospitable, and runs in opposition to our biological makeup. Human beings were molded and shaped on Earth. Space is not that, and it will suck. The people who will be forced into space will be poor people displaced by war, climate change, or some other disaster, in the same way that European immigrants to the New World were the poor and huddled masses. It’s an equilibrium restoring mechanism.

Space is great, and for a full explanation please see the following link: https://www.youtube.com/watch?v=ilcRS5eUpwk

There may or may not be a rebuttal post coming from a space cynic in the coming days.

References:

(1) http://www.astronautix.com/k/korolev.html

(2) https://www.nature.com/articles/355105a0.pdf

(3) https://www.cia.gov/library/readingroom/docs/CIA-RDP80T00246A030100210001-3.pdf

A few weeks ago, Shyam made an interesting point that has been bouncing around my mind. We were in the Union, and after buying an organically sourced soy milk product he said something to the effect of “I don’t want to have to do research about what are good (as in morally responsible) products/companies, I want everything to be already factored into the price.”

While I can’t be certain, and this was not the subject of conversation, I am still fairly confident that the idea of carbon taxes played into Shyam’s comment. Because the Nobel Prize for Economics was recently awarded to two climate economists, I will make this post about carbon taxes. Admittedly, I know little about the two economists who won, so instead I will turn to a research binge I did over the summer on this subject.

Let’s start with command and control regulation. Best available technology (BAT) is any regulation that requires companies to acquire (you guessed it) the best available technology to reduce emissions. A literal interpretation would require a company to acquire the technology or equipment without reference to a cost-benefit analysis. This is uneconomic. More frequently, BATs are interpreted in terms of practicable acquisition of technology, which is a bit of a gray area, and accordingly the policy is less effective. In the US, BAT terminology is used in the Clean Air Act and the Clean Water Act. This is clearly not a comprehensive list of command and control regulation, but rather just one example that is practiced in the context of the US.

Carbon taxes are an example of a market-based incentive away from carbon emissions, albeit a feeble one. Governments can unilaterally decide to implement a tax per ton of carbon dioxide released into the atmosphere. This is an example of a Pigovian tax, a tax used to discourage an activity based on the negative externalities an activity or good produces. Theoretically, the tax should be equal to the negative externality (the social cost) associated with that activity, so that the offending firm internalizes all of the cost. However, this method is largely ineffective. The social cost of carbon emissions is global, and governments only have the incentive to tax the social cost that is incurred within that country. With the exception of Sweden, this is exactly the result that is realized: carbon taxes are set far too low to be effective.

Cap and trade regulations create “tradable emission rights” (or pejoratively, “rights to pollute”) that allow economic agents to trade for carbon emissions in a market. The governmental authority sets a ceiling on what level of pollution is permissible, and then issues permits according to that ceiling. Economic agents can then trade them. This system incentivizes agents to reduce their carbon emissions, since they can then sell them to other agents that are not able to do so.

Additionally, the cost of emitting carbon would be captured in the price of any good that creates carbon emission. Let’s take Union soymilk as an example. It’s unlikely that the producer of that soymilk purchases any carbon permits directly. But it would have to buy transportation services to get its product to market, and it would pay higher prices for these services, as those firms would have to pay for permits or pay more for gasoline. This added cost would ultimately be passed on to the consumer. The emissions associated with that soymilk would be included in its price, eliminating the need for consumers to independently research the emissions effect of the soymilk. This would go for all goods and services.

Let’s suppose there are companies A & B in completely different industries. Let’s assume that technology is out there that will enable company A to reduce emissions by 75%, but at substantial and previously uneconomic cost X. Let’s assume that company B can reduce emissions by only 5% at cost X. Cap and trade in this example would make it economical for Company A to incur cost X and sell its surplus credits to company B (and others like it.) Cap and trade has the effect of incentivizing those agents that can reduce their emissions the most to do so, something that maximizes the effectiveness of emission-reducing spending.

However, there is a substantial need for all countries to implement cap and trade regulation. Without a functioning global market, high polluting agents would be expected to simply relocate to nations that do not tax pollutants. Since the negative externalities associated with emissions are global, this would imply no meaningful positive change.

There are also significant free rider problems associated. If country Z is responsible is responsible for 5% of total emissions, 95% of the benefit of any action it takes to reduce emissions would be captured by the rest of the world. Therefore, there would need to be concerted, global action to avoid free riding nations.

A fun and relevant example of successful cap and trade regulation is that of the EPA’s Acid Rain Program (ARP.) However, a chief difference in this program was that the environmental degradation was local and the United States was thus able to take unilateral action.

I confess to being biased in favor of a cap and trade solution, largely for reasons listed above. I will link a few articles that do not necessarily share my biases and are likely more compelling and informative than what I have shared here.

Here is a link to an article written by Gregory Mankiw that is in favor of carbon taxes rather than a cap and trade system. I found parts of the argument underwhelming, although in last week’s Econversation Shyam made a compelling argument in favor of carbon taxation (although I personally haven’t decided if I prefer it to cap and trade.) With respect to this article, Mankiw makes the point that emission rights might not be auctioned, which wouldn’t be ideal. However, he leaves the argument at that. Additionally, Mankiw doesn’t speak to the global nature of the emissions crisis, which would have to play into any system.

https://scholar.harvard.edu/files/mankiw/files/smart_taxes.pdf

References:

https://academic.oup.com/reep/article/3/1/42/1530330

Jake ElSarhan reporting for Econversations.

In recent meetings, a topic that has been popping up consistently has been that of behavioral economics. For any statisticians following this page, be aware that this is largely due to yours truly biasing the sample by steering discussions to that very subject.

Over the past two weeks, two interesting examples of irrationality have been discussed. The one examined today is that of hyperbolic discounting. To begin with, let’s imagine that a student named Marisa has been offered the choice of $100 now or $200 in one month. What is the rational choice? Why? What is the more common choice? Why?

Before we get into that, I need to clarify the difference between discount rates and discount factors. A discount rate (r) refers to the interest rate that is used to determine a net present value (NPV) from a given set of cash flows. For businesses, r would be determined by weighted average cost of capital, for individuals it might be the cost of borrowing. Generally, the discount rate is determined by market/economic factors.

In economic analysis, the discount factor (beta) is the measure for how people value time. The most basic form of a discount factor is 1/(1+r). The r chosen for the discount factor can include more abstract considerations, such as need for resources, and psychic (as in psychological) considerations. When implicitly calculating the psychic utility gained from $100 now or $200 in one month, the discount factor is what compares the figures. Different people will have different discount factors, and the r in the denominator is typically quite high, far higher than the market interest rate.

Obviously, the rational choice is $200 in one month. The NPV of $200 a month from now is considerably higher than $100. However, repeated studies demonstrate that the more common choice is $100 now. (“Not me Jake! I’d choose $200 in a month!” That’s the great danger. Studies show this bias affects you. So does advertising.)

The reason for this is that people have an ingrained focus on the present at the expense of the future. To borrow the terminology of Professor Baker, we might say that we make decisions using an excessively high discount rate, maybe 30 or 40 or 500%. Thus, taking the $100 today becomes rational, even though the market discount rate might be only 8% or something.

Here is where it gets interesting. If we asked Marisa if she’d rather have $100 in 12 months or $200 in 13 months, she’d probably say $200 in 13 months. This is rationally incompatible with the former example, but it can be expected given what we know about human nature. Therefore, we can say that humans engage in hyperbolic discounting which is when valuations fall very quickly for a short period of time and then level off. This is inconsistent and a large part of behavioral economics.

What explains this? The constant battle between the amygdala and pre-frontal cortex. The amygdala is standard for mammals, and is responsible for baser functions, and takes over in moments of immediate crisis, like fight or flight. It governs our reaction to our immediate circumstances and short term thinking. The pre-frontal cortex is uniquely developed in humans (even among primates) and is responsible for long-term thinking and so-called rationality.

To put it simply, the amygdala is why people have a tendency to take $100 now over $200 in a month. If you start thinking hard about it and decide you’d rather have the $200, that’s probably the pre-frontal cortex taking over. When confronted with a situation far into the future, it’s the pre-frontal cortex that is calling the shots. This explains hyperbolic discounting. This is a real science, it’s called neuroeconomics.

Next time, we’re going to examine a hypothetical individual named Shyam who chooses $100 both times. I fear the answer will have to do with consistency in an attempt at self honesty (is that a word,) and that it will be a fascinating analysis having to do with an overdeveloped pre-frontal cortex insisting on perfect harmony with the amygdala.

References:

https://pubs.aeaweb.org/doi/pdfplus/10.1257/aer.99.3.937

https://pubs.aeaweb.org/doi/pdfplus/10.1257/aer.99.5.1925.

A few weeks ago, Davidson had the honor of having Dr. Joseph Stiglitz come visit campus to deliver the annual Cornelson lecture. Besides offering the opportunity to hear from one of the most respected and experienced economists in the world, one of the most exciting parts of Dr. Stiglitz’s speech was how his topics relates directly to what we’ve been talking about in Econversations lately. I guess Davidson students are smart, because we’re interested in the same stuff that is interesting a Nobel Laureate. So, I’d like to take a little bit of time looking back on how Dr. Stiglitz shed more light on some of the subjects that I’ve written on over the past couple of weeks.

Costs of Inequality

When I wrote about the “Lost Einsteins” paper, I commented on the massive waste of potential inequality causes as a universal economic consequence, over and above the inherent costs of inequality to the individual (and therefore, to those concerned with inequality as a purely social, and not economic, issue). Dr. Stiglitz spent a fair amount of time during his presentation expanding on the real damage inequality does to the overall macroeconomy.

Dr. Stiglitz referenced the book Efficiency and Equality: The Great Tradeoff, by well-known, and well-respected, economist Arthur Okun. The theory that Okun puts forward in the piece does hold water, or rather, in this case, aptly does not. Okun posits a “leaky bucket theory” that says that redistributive efforts bent on easing inequality automatically come at a cost of efficiency: administrative costs of redistributive agencies and regulatory activity, decreased incentive to work at higher income levels due to higher marginal tax rates, and an increase in effort to avoid taxation through creative tax shelters or deductible spending. At the very least, he’s certainly not long about the black hole of bureaucratic inefficiencies, and just last week Shyam mentioned that studies have documented the instinctual human behavior to begin gaming rules as soon as they are set. I have some qualms with the argument about deductible spending, because, ostensibly, we include tax deductions in an effort to encourage certain forms of spending (such as investment or charitable contribution), but nonetheless, Okun’s points are well taken.

However, what Okun fails to take into account is that, quite frankly, all the money in the world can’t buy you a solid bucket. To step away from the metaphor for a moment because I think we are starting to stray from the point, Okun’s theory assumes that the current state of affairs is more efficient than a more redistributive system. Dr. Stiglitz provided data and theory to demonstrate that inequality is not the consequence of efficiency, but rather inefficiency is the consequence of inequality.

The chart below shows that in the last 60 years, corporate profits as a percent of GDP peaked in 2013 at 11%. The chart below that shows that in the last 60 years, private business investment peaked in 1966 at 28%.

Both charts are from Dr. Stiglitz’s powerpoint slides, which he was kind enough to share with me, and use data from the Federal Reserve Bank of St. Louis. I’m only taking into account the data from 1960 onwards, since that’s when the data for business investment starts.

For comparison, in 1966, corporate profits constituted 7% of GDP, and in 2013, business investment constituted 11% of GDP.

So, in the peak year of corporate profits as a percent of GDP, corporate investment as a percent of GDP was 17 percentage points lower than it was in its own peak year. In the peak year of corporate investment as a percentage of GDP, corporate profit as a percent of GDP was 4 percentage points lower than in its own peak year. Effectively, businesses are profiting more but they are investing not just slightly less but significantly less. Moreover, if you look at the data points surrounding 2008, things get even more interesting. First of all, I swear even on graphs recessions look scary. They get all pointy and so it looks either like a cliff you could fall into or something sharp and stabby. Which, you know, is really apt considering their exceptional ability to ruin lives and cause mass chaos. But secondly, by July of 2009, corporate profits constituted the same portion of GDP as in July of 2007. In 2009, business investments constituted 3% of GDP, compared to 13% in 2007. Business investments still have not yet returned to 2013 levels, reaching only 12% in 2015 before declining again.

These data points show that even though company profits are becoming a larger part of the economy as a whole, companies are sitting on their profits instead of spending them. Investment is a key driving force in the economy, not just because money firms invest is distributed throughout the economy, but also because investment increases production and, more often than not, increases efficiency.

Were Okun alive today, he might not even disagree with Stiglitz. For his leaky bucket theory, Okun is considered one of the leading supply side economists, subscribing to a central belief that high marginal tax rate “discourages income and output” which ultimately slows the economy. Importantly, the negative effects of high marginal tax rates happen at both ends of the spectrum. As I mentioned in my post on the UBI, certain welfare policies that specifically apply to certain income levels make the marginal tax rate at the threshold for the policy extremely high.

However, high levels of income are actually in and of themselves discouraging output. As Dr. Stiglitz explained, much of the current inequality is caused by rapidly increasing market power. Firms with a lot of market power have no incentive to invest because doing so would simply cannibalize their own business. Because they are already producing at, or close to, their profit maximizing point (see my post on social surplus for an explanation of why that is), any investment to increase output would make their marginal return less than their average return (effectively, the amount that they would make on producing the next unit is less than the amount they currently make per unit).

I’m actually reminded of one of the Juan Bobo stories my mother used to read me as a child. For those who don’t know, Juan Bobo is young boy who is a central figure in a lot of Puerto Rican folk tales and fables. This is the collection of retellings I had as a child.

In one of his stories, Juan Bobo’s mother instructs him to get water from the stream near their home. When Juan Bobo protests that the buckets his mother has given him will be too heavy when filled with water, she suggests that he find something else to carry the water. Juan Bobo selects two wicker baskets, and goes down to the stream as he has been instructed. When he returns to the house, he excitedly tells his mother that he believes he is getting stronger: the water seemed to grow lighter and lighter as he walked (this story also reminds me of last week at the gym when I thought a workout was getting easier and then I realized I was doing it wrong, so it just goes to show the power of fables in relating to your life I suppose).

Anyway, the story continues as follows:

“’That is odd,’ said Mama. Then she stepped into a big puddle!”

These rising corporate profits are giving the illusion that the economy is growing stronger, but the growth is so concentrated that the economy at large is not benefiting the way it could be were the resources more evenly distributed. Instead, the very wealthy have these wicker baskets that are refilled as fast as they are draining, and the rest of the country is left with a big puddle and no water for washing the dishes.

The only problem is, we aren’t dealing with water to wash the dishes. We’re dealing with the money that people need to fill the dishes with food in the first place. No matter how much I zoom out to say that even if you don’t consider the individual, inequality is bad for the economy, I want to make sure I’m zooming back in and reminding myself, and you, to think about the individual as well.

Innovation

So most of you have probably heard of the trolley problem. But for those of you who haven’t, it goes like this: you are in an out of control trolley careening toward five people on the tracks. You cannot stop the trolley, you cannot get the people out of the way. The only thing you can do is operate a track switch. If you switch tracks, you will head down a track with only one person on it.

Many people will respond, “well, if you switch tracks, then you are killing fewer people, so you should switch tracks.”

“But,” whoever has posed the question might ask, “what if the one person will go on to cure cancer?”

Besides really hating the person who asked because you didn’t sign up for this thinking through your fundamental ethical beliefs nonsense, the moral of the story is that people’s potential matters. That the capacity to innovate matters.

The economy still has major barriers to innovation. One such barrier is resistance general resistance to change. A central consequence of innovation is a concept known as creative destruction, which essentially the idea that creation and destruction are not necessarily opposites, or mutually exclusive. Sometimes to create something, you have to destroy the components, and sometimes, creating something replaces something else. Invention is revolution.

Think of it this way:

SELF-DRIVING CARS!!! NEATO!!!! THINK ABOUT HOW MANY ACCIDENTS THAT COULD PREVENT IF WE TAKE HUMANS OUT OF THE EQUATION!!! TECHNOLOGY IS SO COOL!!!!

Unless you’re a truck driver, a cab driver, an uber driver, etc.

AW, MAN NETFLIX IS THE BEST. THAT WAS TOTALLY INGENIOUS AND A GREAT THING FOR EVERYONE.

Except Blockbuster.

Think about what AUX cords did to radio, what iPods did to CDs, and for that matter, what CDs did to records.

Some resistance to creative destruction is cultural. Policy makers might not support public investment in automation technologies that would be unpopular with their constituents, or alternative energy research in areas whose main industries are mining, fracking, or drilling. Interestingly, countries like Sweden that have expansive social welfare systems are significantly more pro-innovation because they are unafraid of job loss. Peter Goodman reports in the New York Times Magazine that 72% of Americans are “worried” about robots and AI, while 80% of Swedes have positive views on the subject. The Swedish system, featuring large unemployment benefits and comprehensive job training makes people feel secure. That said, many economists fear that we are approaching a precipice: a wave of mass automation that could overwhelm even the social safety nets as large and in depth as the Scandinavian systems. Essentially, we have to face down the reality that the destruction might be faster than the creation.

Some resistance to creative destruction is simply economic reality. Economies of scale are a huge factor for almost any innovating industry. Think about how much money goes into pharmaceutical R&D. Think about the kind of facilities and equipment you need, the kind of relationships with insurance companies you need. Competing with a pharma giant is really hard. Think about a social network that already has a huge user base. Any new social media site or program has to draw that kind of interest before they can start profiting through ads and data, which are the major revenue streams for social networks. Cost wise, competing is unbelievably hard. Those companies also have to convince potential customers to move away from companies with significant brand recognition, brand trust, and market power, often in a saturated market.

Sometimes those corporate giants actively combat creative destruction, either by buying out startups early on or by trying to create legal barriers.

Creative destruction can also be stalled through illegal means. For instance, dumping is the illegal practice of flooding the market with goods being sold below costs by companies who can afford to take a loss, which forces other businesses out of the market and effectively makes the firm a monopoly—who can now gouge prices. In a surprisingly applicable but totally fictional example, last week’s episode of DC’s Legend’s of Tomorrow, set during the cold war, some oil tycoons hired an assassin to kill a scientist who had discovered cold fusion because it would have put them out of business. So you know, not terribly realistic, but it gets the rationale across.

In addition, we have a major issue strangling innovation that is far more subtle, and, in my opinion, far more concerning. A study from the Equality of Opportunity Project, lead by Raj Chetty and his merry band of high profile economists, shows appalling results about who is likely to become an inventor (the full study is here, and a summary article is here). Using third grade math scores as a proxy for general skill, the study shows that overwhelmingly the inventors are rich, white, and male, regardless of their aptitude. While high aptitude children of high socioeconomic stature were significantly more likely to become inventors than lower aptitude children of the same income class, high and low aptitude children from low income families were equally likely—or unlikely, as the case may be—to innovate. The study also showed the importance of role models: children who grew up in cities with a lot of innovation were more likely to become inventors, and a large number of existing female inventors in the city increased the numbers of future female inventors in that area(the same goes for men). These results may be extrapolated to suggest the importance of representation to inspire people with a myriad of goals, not just young inventors.

The income gap in innovation likely has a number of explanations. The first major explanation that I can think of is risk. The ability to take on risk is a high-income privilege; if a person always knows they will have the money to eat and pay rent, they can dedicate time and money to an endeavor that might fail

The second major issue is access. Children who grew up in high-income families have significantly more educational opportunities. They also are more likely to have familiarity with systems of capital or a support network to help manage those systems. They are more likely to have seed money and a much more ready ability to source a “friends and family” investment round.

Chetty and his colleagues call these children “Lost Einsteins.”

The funds that have helped me develop this project are through the Davidson Innovation and Entrepreneurship program, which is just one more example of how privilege can afford innovation. Just think about how many people are smart enough to be sitting where I am right now. On my bed, in my campus apartment, working on a project that I’m passionate about, running late because I want to finish this thought. We’re losing out. Big time.

The UBI is a controversial “new” idea in economics that is considered both a way to encourage invention and protect from it. Though the UBI has been in the news lately as business leaders in Silicon Valley are championing the policy in the hopes of easing the transition for those technology will put out of work, the concept is not new. The idea, favored by the likes of Thomas Paine (whose Common Sense is now perhaps best known as what Angelica Schuyler has been reading), Martin Luther King Jr, and Chicago school economist Milton Friedman (best known for the monetarist theory) is not new.

And, of course, the controversy is not new either. As with any government payout, the UBI causes concerns about the “free-rider problem,” i.e. people who could be working do not because they are content to live off of government handouts. That said, I’m inclined to think that we would not see a pandemic of non-working Americans. First of all, capitalism is driven by individuals striving to attain a certain level of luxury. Many people in this country work crazy hours and have little time for leisure because they have to in order to survive. But many people also work crazy hours with little or no time for leisure because they want the money that comes with it (I don’t think anyone goes into investment banking for that great work-life balance it provides). People will still work hard. People will still have passions to pursue and luxuries to strive for and, honestly, you can only watch so much Netflix before you need to do something else.

Shyam believes, similarly, that we won’t see a huge drop in labor force participation because of simple, evolutionary human nature. People are naturally competitive and we naturally (for better or for worse) tend to measure our success by the success of others, be it in terms of wealth, achievement, or personal life successes. That nature cannot be overwhelmed in one fell swoop.

University of Chicago Economist Iona Marinescu compiled data on a number of UBI-like programs to compare the results and extrapolate to the impacts of potential future policy options. The closest program to a full UBI is the Alaska permanent fund, which pays out small dividends of about $3000 to all citizens of Alaska. Her data shows no shift in overall labor force participation save a small shift from full time to part time workers. She says that while the results may be different with a larger transfer, say, at the poverty level, the increased aggregate demand would drive a larger increase in labor demand that would counteract those effects.

The unique particularities of the UBI offer a lot of technical advantages:

Universality and Unconditionality

One of the reasons that we don’t have more empirical information to predict the effects of the UBI is that most programs affect only a specific portion of the population that meets a given condition. Conditional programs are susceptible to a lot of inefficiencies:

Critics of current welfare programs, according to Marinescu, say they contribute to poverty traps. If we condition cash transfers or program eligibility on a certain level of income, then making 1 extra dollar can move a person over the eligibility threshold and cost them severely. Thus, marginal tax rates are actually the highest on the very poor, where a very small change in income can cost a lot. For those individuals, every time they get close to surfacing from poverty, the rug is pulled out from under them.

Often unemployment benefits are given a set time limit, the idea being theoretically to make sure that people do not take advantage of the policy. However, sometimes, there are simply no jobs to be found, and then these policies fail to protect those who really need them. Many attempts at foreign aid are also not having the intended impact. According to a New York Times Magazine article, recent studies have shown that programs like PlayPump are not effective in increasing access to clean water, while microfinance and skills training are expensive with little affect on stability or poverty.

Many programs that are conditional lead to inefficiencies because they force people to make choices they otherwise might not have, such as taking a job that is not right for them or spending a certain way. Even if a program is effective, is it the best way to be helping people? The same NYT Article sites an executive of a relatively young nonprofit, GiveDirectly, asking ““Could you imagine sitting in an office in London or New York trying to figure out what this village needs?” An active participant in the ongoing debate about the efficient use of money, GiveDirectly has been exploring the UBI as a better alternative to many foreign aid endeavors. The article, titled(I think rather inappropriately, as it offers little evidence of shrinking labor supply) “The Future of Not Working,” follows the GiveDirectly executives through Kenya as they roll out their plan in pilot villages to measure its effects. Anecdotal evidence suggests that the program would be effective: many of the recipients’ spending decisions are entrepreneurial in nature, or they are spending on basic needs such as food, better roofs, or even paying down a dowry. Lowrey also notes that many proponents of the UBI think that it could have the most impact in the poorest regions.

Labor Force

I believe that the UBI will affect labor supply, but I don’t believe that the UBI would shrink the labor supply. Instead, the program would make the labor supply much more elastic, and which could be huge for workers. For those of you unfamiliar with the concept of elasticity, the quick and dirty explanation is how responsive you are to a change in price. You can literally think of price elasticity like ratty sweatpants versus skinny jeans. Ratty sweatpants have an elastic waistband (see what I did there), so if you gain some weight the sweat pants will move in response. When something is price elastic, the demand moves in response to a change in price. Your skinny jeans on the other hand, are not budging if you gain weight. I think you see where the metaphor is going. Goods traditionally considered relatively inelastic are things like medication, food and water, and other necessities. That should make sense if you think about it: if the water company raises the price of providing running water to your home, you’ll probably still pay for it unless you truly can’t afford it. Relatively more elastic goods are things that people can live without, both in the literal basic need sense, but also in the more colloquial “okay, I can live without splurging on this” sense. Whatever your typical non-necessity spending is—clothes, eating out, video games, Netflix, extra lives on candy crush—if the price goes up, you might be more inclined to buy less of it. The concept applies to supply as well: some producers will lower supply a lot if the price drops, and some producers will not lower supply very much at all. One reason for that is the cost structure: if producing a good has a lot of variable costs (i.e. costs that are incurred with each unit of production, such as source materials or hiring an additional hour of work) a good will be more responsive to price changes. If a good has a lot of fixed costs (costs that are incurred no matter how many units are produced, i.e. factories and equipment) then the change in price will not cause a major shift in quantity supplied. Firms with high fixed costs need to get a certain amount of revenue to cover those fixed costs or they’ll have to go out of business.

In terms of labor supply, you can almost think of a worker as a firm with high fixed costs. Food, water, shelter, clothing, electricity, student debt perhaps. At a certain point, they have to sell a certain number of units of their labor to cover their fixed costs (i.e. survive). For that reason, labor supply is extremely inelastic, particularly at the lowest end of the income distribution, which means that firms have an inordinate amount of power over workers. Minimum wages and unions are two examples of strategies employed to protect workers, but minimum wage doesn’t really give workers bargaining power of their own and unions are controversial and do not protect everybody.

The UBI could give workers the ability to say “no” in a way they never have before. It allows for the possibility of a fair market solution as opposed to interventions to correct market failure. The impacts would be not just on wages but on a lot of other workers rights, such as legally mandated break times, paid sick leave, maternity leave, vacation, and exploitative policies such as split-shifts or on demand scheduling. I strongly believe that we are looking at a possibility to give a market absolutely riddled with market failures the chance to reach socially optimal conditions. (By the way, market failures are one of my very favorite topics in economics so BOLO for a post on that). Though it will almost definitely mean firms will have to pay higher wages, labor demand should increase as demand for goods and services is spurred upward by the stimulus of the UBI. Not only that, but the evidence of who benefits from economic growth is staggering: given workers bargaining power would ensure that increased profits from that increased demand is actually passed down to the worker instead of being absorbed by the company.

Innovation and Externalities

Among the most commonly cited benefits of the UBI is its capacity to encourage innovation and invention, either by assuaging fears of mass automation or by giving people a literal safety net to go out on a limb and try to start something new. Just as people will have the opportunity to say no to jobs that are not offering fair wages or conditions, people will also have the ability to leave secure sources of income in favor of entrepreneurial endeavors without the risk of losing everything. The UBI would very likely help correct the major income bias of the “Lost Einstein” phenomenon and encourage innovation and risk taking, which is very healthy for economic growth. The UBI would also encourage people to go into industries with high externalities whose wages do not match their value to society. For example, as romanticized as the “starving artist” trope is, the opportunity to pursue an artistic path is definitely not open to everyone. Huge sums of money, governmental and nongovernmental, go toward supporting the arts or artists in various ways, so we know that the production of art is something whose social value exceeds its market value as well. While the arts are the typical example of the underpaying career (unless, of course, you make it big), plenty of other careers provide benefit that significantly outweighs their compensation. Becoming a social worker, a public defenders, or a doctor in rural area requires an advanced (and expensive) degree and a buildup of debt and expenses that make these careers infeasible for many qualified people. Non-profit work is another example that many people would elect to do given the basic income to supplement the relatively low salary.

Drawbacks

So, clearly, I think the UBI has incredible potential. I really support, at the very least, continuing to explore the possibility. With any economic policy, even if one with a lot of theoretical capacity to do some good, you have to figure that it has an extraordinary capacity to destroy everything. We need to be skeptical always. The whole “trust, but verify” thing is never, ever a good, or even viable, idea in economics. Do not trust until you have tried really, really hard to verify, but also know that you probably will never totally be able to verify because you can’t control for everything that is happening in the world to isolate effects. I have spent a really long time trying to think through the issues posed by the UBI, and the following are a few I’ve come up with.

It’s not a fix-it-all

The UBI is essentially justified by the idea that people are the best judges of how allocate their resources (both money and time). I have just spent a lot of time enumerating the ways in which the UBI could help a free market function better, particularly in the labor market. But we will never ever exist in a world in which markets are single-handedly capable of reaching optimal solutions by almost any standard of optimality.

Many who are considering the UBI in a country like the US are viewing it as a replacement for all other forms of welfare policies and social safety nets. A GiveDirectly executive said, “if half-jokingly: If cash transfers flourished, ‘the whole aid industry would have to fire itself.’”

A recent IGM panel on the UBI asked a variety of economists to respond to the following statement: Granting every American citizen over 21-years old a universal basic income of $13,000 a year — financed by eliminating all transfer programs (including Social Security, Medicare, Medicaid, housing subsidies, household welfare payments, and farm and corporate subsidies) — would be a better policy than the status quo.

Only 2% agreed. With 19% uncertain, the other 79% of panelists disagreed or strongly disagreed. In other words, approximately the same proportion of dentists who recommend trident to their patients who chew gum don’t think the policy outlined above is a good idea. While some economists disagree on principle with the UBI, (“Bill Gates would get 13K, which is crazy”—Oliver Hart, Harvard; “Some people eligible for welfare choose to not apply, making this proposal unnecessary.” –Kenneth Judd, Stanford) the majority of those who chose to leave comments with their vote had concerns about the replacement aspect (or other specifics of the plan).

For instance:

“There is much to recommend a universal basic income, but specifically a 13k income while ending all other transfers is difficult to assess.” –Larry Samuelson, Yale (vote, uncertain)

“A properly designed negative income tax could be part of a better policy, but replacing everything is a bad idea.”—Richard Schmalenesee, MIT (vote, disagree)

“The simplicity is attractive, but deceptive. Coupled with universal health care & tax reform it could work. but we are far from that.” Christopher Udry, Yale (vote, disagree)

“Total health expenses and risk will remain high for individuals…” Marcus Brunnermeier, Princeton (vote, disagree)

Many also commented that $13,000 was not nearly enough to live on, or criticized the fact that it was only for persons above 21 years of age (and therefore not universal, and also causes problems for families living on the same income with several children). However, what the economists above pointed out is that specific, targeted government welfare intervention is still crucial. The healthcare market, for example, is one of the markets most susceptible to failures and inefficiencies, and trying to treat the UBI as a magical replacement for everything else would definitely be a mistake.

Similarly, in the context of GiveDirectly and foreign aid, we need to particularly bear in mind limits of infrastructure, technological capacity, and governmental systems of developing countries. For countries without a strongly developed insurance industry, or with large populations that cannot access that system, targeted medical aid, such as the delivery of medication or the services of medical professionals make a huge difference. Many of the aid organizations also target specific demographics: for example, some are specifically focused on empowering women in different regions. The danger with the UBI is thinking that it can erase all the other shortcomings of a free market economy. And since we can’t use it as a replacement for current spending, at least not entirely, then how do we finance the program?

Lack of Empirical Data

Although Marinescu’s report does cover a lot of ground and show early promise, none of the currently running experiments constitute a full UBI. The closest, the Alaska Permanent fund, is a transfer of $3,000; I don’t think we can reasonably extrapolate labor market effects from a transfer of $3,000 to a transfer at a living income. If anything, the shift from full time to part-time work is disconcerting because it suggests that given the income, people will work less, but the amount is not high enough for them to leave work altogether. Meanwhile, the Roosevelt Institute found in a study that a $1000 a month UBI would increase GDP Growth by 12.56% over 8 years if financed by government debt and 2.62% if financed by increased redistributive taxes. They also say that the UBI would ultimately decrease federal deficit. Once again, you can find the full report here, or summary information here. First and foremost, I never believe growth projections. Unless you’re Raven Baxter, Alice Cullen, or Sybil Trelawney, I don’t want to hear it, and honestly I’m pretty sure macroeconomic indicators for the better part of a decade are outside their psychic scope anyway. I know that growth projections are used in a lot of important decisions in a wide variety of fields, but frankly I’m not sold. I’m also healthily skeptical of any program that aggressively increases government spending and promises to reduce the deficit. Don’t get me wrong, the theory to back it up exists: the resulting stimulus leads to government revenue that outweighs the increase in expenditures. My problem is that the UBI requires continuous payments and many of the stimulating results will not kick in right away. Supply cannot always respond as fast as demand can change, the presumed innovation effect will need time to take root and flourish, and the transition period in the labor market might cause a small hiccup in productive capacity. None of these mean the UBI doesn’t make sense and that the economy won’t get beyond these bumps in the road, but they do require us to be skeptical about promises made by supporters of the policy. All I can say is this: without a whole lot more data, if they do instate a UBI I can promise you nothing except the money they decide to give out and that I will be watching the drama on capital hill unfold with a giant bowl of popcorn.

How Much To Give

The Alaska Permanent Fund is $3,000 annually. The amount suggested by the Roosevelt Institute is $12,000 annually. The amount suggested in the IGM question is $13,000 annually. None of these amounts represent a living wage. I am not confident that transfers in these amounts will have the same positive effects outlined above: workers may not have as much bargaining power if they can’t make a living without work, and innovators won’t take risks if their safety net is not strong enough to catch them. Of course, a policy that tries to approximate a living wage will be significantly more expensive and poses more risk of a shrinking labor force. We also need to consider wildly fluctuating costs of living and whether we can find a “one size fits all” optimal income.

Inflation

Theoretically, aggregate supply should move to meet aggregate demand, which should keep prices relatively stable as the UBI goes into effect. I absolutely believe that overall aggregate supply (or total productive capacity of the economy) will increase which would push price levels down, but I worry that supply can’t change as fast as demand and we will see, at least in the short run, a fair amount of upward pressure on prices (although one way to mitigate this would be to create a significant lead time between the passing of the UBI and the release of payments, which would give producers time to gear up). Regardless of the impact of the policy itself on prices, inflation will come. If the UBI is given at a discrete, nominal value, be it $3,000, $13,000 or $30,000, then we might run into the same problem we are having with minimum wage: the wage level was set 11 years ago and is constantly a source of political debate. If the UBI amount is not responsive to inflation, we will very likely start to see the positive effects of a universal income (increase in consumer demand, increase in innovation, increase in optimal working situations) decline.

No Going Back

If you think raising taxes is unpopular for a politician, try finding one excited to tell everyone that they will be actively taking away a significant, steady source of income. If we put a UBI into affect, odds are we are going to have a very hard time getting rid of it. Basically, we’d better be sure it’s really going to work.

This season’s Big Bad

I watch a lot of DC Comics TV shows, so sorry if the whole ‘big bad’ framework is too nerdy for you. That said, you are spending what is presumably your free time reading an economics blog and I have never pretended not to be nerdy.

Monopoly and Monopsony

How many companies do you think would wish they were big if they encountered Zoltar? (For those of you who have no idea what I’m referencing, it’s a 1988 movie called Big starring Tom Hanks and you should definitely watch it). Here’s the problem: a big company has market power. Market power, by simple economic definition is how much capacity a firm has to drive prices, but the concerns go far, far beyond that.

First and foremost, market power causes market inefficiency and deadweight loss, as well as redistributing surplus from producers to consumers. For those of you who don’t know, or need a refresher, on deadweight loss and consumer and producer surplus, check out this post.

Even though monopolies are not ideal, if a luxury good is produced by a monopoly, that’s not such a huge deal, at least in terms of social impacts. However, one of the most common industries for monopolies, if not the single most common, is pharmaceuticals because they are granted patents. I’m not saying that patents are inherently a bad thing; astronomical amounts of money go into the creation and testing of new drugs. I worked in branding last year and you’d be surprised how hard it is to even name a new medication (if the name is too similar visually or aurally to something on the market, dangerous medication errors can occur).

If we didn’t grant patents there would be no incentive to put in the research and development money if someone else could just use the formula as soon as you finished it. While some policy makers are seeking alternatives to incentivizing R&D, patents remain the prevailing strategy for the time being. So, yay R&D! Except, remember that time a guy who would later be referred to as the “most hated man in America” raised the prices on an AIDS medication from $13.50 to $750 a tablet. Nobody can sell that drug for cheaper, so anyone who needs that medication needs to pay up or face major health risks.

A company doesn’t have to have full-blown monopoly power to have a dangerous level of market power. The more market power a firm has, the harder it is for other, smaller firms to compete.

Another major issue with huge companies is monopsony power, which by economic definition is a company that is not facing competition for the purchase of inputs (where labor is an input to be purchased) (to be clear when economists talk about purchasing labor, they mean purchasing a service from the “seller” who is the individual worker). Often, monopsony denotes a firm that is a single employer for an area or group (though it can also denote a firm that is the only client of a given capital producer). Again, even if a company does not literally employ every single person in an area, they can still have dangerous market power. Just like a monopoly prevents consumers from seeking a better price or product elsewhere, a monopsony prevents workers from seeking a better job or salary elsewhere. As I mentioned in my post on inflation, one issue caused by sticky wages is the continual redistribution of income to profit-earners instead of wage earners. In October 2016, the Council of Economic Advisors released a brief on monopsony power, with one key argument that monopsony is helping to drive such redistribution. The brief also points out that, as monopoly power drives prices upward while driving quantity downward (thereby productivity and creating that deadweight loss), monopsony power drives wages downward and number of workers hired downward. In terms of social impact, we not only have larger unemployment, with even those who are employed making a lower wage than is optimal, which can slow down economic growth in a number of ways, we also have lower output. Going back to the very basics of supply and demand, less output means a higher price for consumers. Also, the impacts of inequality pose major issues to economic efficiency, a subject I could easily dedicate an entire—or several entire—posts to discussing.

The issue of incredibly powerful firms goes well beyond the traditional goods and service markets or labor market impacts of standard theory and discussion. The issues posed by Amazon, which The Seattle Times says has turned Seattle into “America’s largest company town,” have little to do with their power over their employees. Amazon workers, who are typically high skilled, high paid workers, are not necessarily the ones suffering. “What was once a quirkily mellow, solidly middle-class city now feels like a stressed-out, two-tier town with a thin layer of wealthy young techies atop a base of anxious wage workers,” Paul Roberts writes for Politico. Seattle also is experiencing overwhelming traffic problems and major rise in housing prices.

To be clear, I’m really not trying to make Amazon the villain. I am not convinced that I would have survived this long without my Prime account, and the ability Amazon has given me to be both lazy and cheap at the same time is truly a gift. But Amazon is still a for-profit company, and they are going to do what they can within the bounds of ethics and a degree of corporate social responsibility to have the highest possible bottom line. Even assuming total benevolence on the part of the monopsony too large a corporate footprint puts too many eggs in one basket. In fact, Seattle had that exact problem in the 1970s when Boeing was the single dominating force. As a New York Times writer describes it, some “worry that the city could become too much of a one-company town, the way it felt in the old days when Boeing would sneeze and the city would pull up the blankets and stay in bed.” I’m not even going to consider the post-apocalyptic nightmare of a Prime-less world, but, even if Amazon, like Boeing, takes a hit but lives to tell the tale, Seattle could still be in major trouble.

Monopsony companies also have undue power over governments, which is really scary when you think about it. The issue isn’t just employment: Amazon owns 19% of Seattle’s office space. That’s as much as the next 43 companies combined. To be clear, that’s also the next 43 largest companies, so Seattle wouldn’t just have to bring in any 43 new businesses to make up for a loss of Amazon. Seattle is also undergoing major public works projects to deal with the new found traffic problems caused by Amazon. More people means a larger taxable base: if you lose that population you’re now paying for a project with money you don’t have for people who aren’t there.

The resulting power manifests itself, in the case of Amazon, through cities bidding to be the home of HQ2, or Amazon’s second headquarters (a dubious blessing according to Seattle, but certainly an in demand one). A New York Times article basically describes the “wooing” of Amazon as an exercise in Peacocking by cities (238 of them, to be exact). Your taxpayer dollars are hard at work funding a viral video of the Mayor of DC talking to Alexa, the transportation of a 21 foot tall cactus 1,538.9 miles (thanks google maps!) via flatbed truck, from Tuscon to Seattle, and ads from the city of Calgary promising to fight a bear to get Amazon’s headquarters (I am at present unclear as to who exactly will be fighting the bear, whether any actual bears will be harmed in the courting of this company, and if so what animal rights group I should contact). Yes, that’s right, you heard it here first, forget habitat destruction and global warming, monopsony companies are what’s really hurting our wildlife.

Joking aside, Amazon has requested that each city include in their application tax breaks and incentives that the city would provide. My own home state of New Jersey offered a 7 billion dollar tax cut to get Amazon into Newark. I’m already a little concerned at that prospect, honestly, because I’m thinking I’m going to start flying into the airports in New York City proper, because the traffic to get home from Newark Airport is going to be insane. Of course, that’s totally speculative on my part, but if Seattle is any indicator, the line of thinking is at least legitimate.

All of that being said, Amazon is not the most concerning example of monopsony, it’s just relevant given the recent news surrounding the company. Where monopsony poses a huge threat is in developing countries. I do want to start by saying that I am focusing on the concerns about monopsony, but having large companies invest in a developing area has advantages, including but not limited to employing impoverished populations, increasing inflows of capital and expertise, fueling growth. The problem is that a company large enough to bring with it huge benefits has huge power, and that is always going to pose risks.

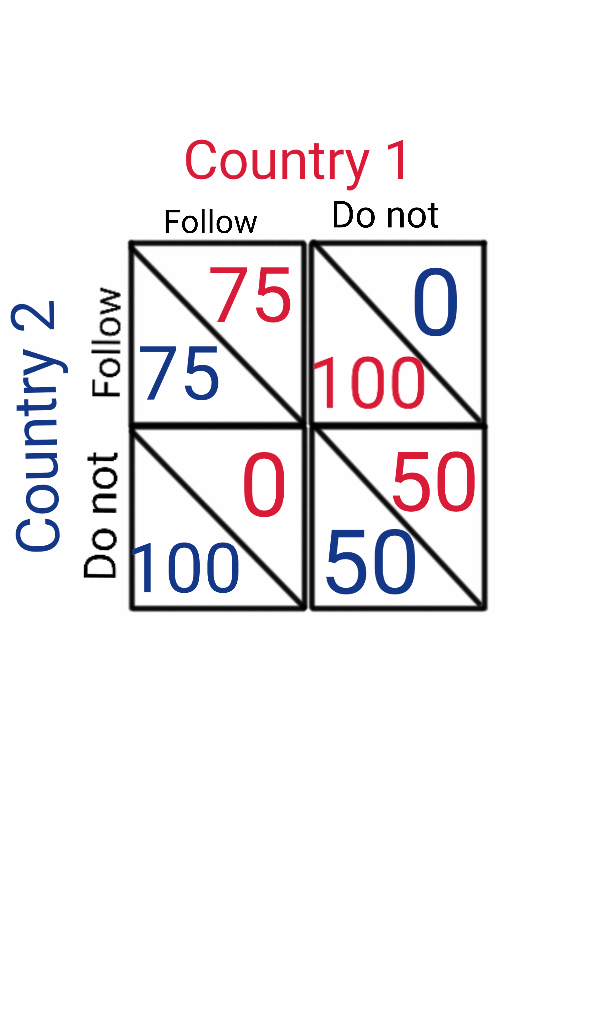

The way I normally think of the issue of monopsony in a developing region is through a game theoretical model, which a lot of you are probably familiar with, called the prisoner’s dilemma.

Suppose the UN passes a resolution on environmental standards, work conditions, tax levels, and wage levels, and recommends that all countries abide by those standards. Simplifying the model to two countries, suppose each one of them has to decide whether to follow those guidelines or not. The prisoner’s dilemma model can apply to any situation in which a binding legal agreement is not possible. Because of issues of national sovereignty, even if every nation agreed to the guidelines (which we must assume for the model to be relevant at all), they are extremely difficult to totally enforce (I did Model UN for years in high school and first of all, TNCs or transnational corporations with monopoly power were a topic all the time and second of all the words national sovereignty were thrown around so much that I am just glad I wasn’t 21 yet because turning it into a drinking game might have killed me).

In this model, you have country one and country two. If both countries stick to the guidelines, then the monopsony corporations will split evenly between the two, and they will both get a payoff of 75, giving a total payoff of 150. If one country does not follow the guidelines, however, and makes doing business in their nation cheaper, the business will flock to their country. They will get a higher payoff, and the country that did follow the guidelines will get nothing. If both countries choose not to follow the guidelines they both only receive a payoff of 50. They still get the benefits associated with the monopsony presence, but they get less because they are unable to regulate at the optimal level. Unfortunately, at least according to the theory, that 50,50 point is the outcome we get.

If country 1 knows that country 2 will follow the guidelines, they stand to make more by ignoring the guidelines. If country 1 knows that country 2 will not follow the guidelines, then if they follow the guidelines they will get nothing. So not following the guidelines is what is called a dominant strategy. Basically, no matter what the other player does, your best option would be to do the same thing. Now lets step back again and think of this in terms of 20 or 30 nations and all of them have to agree totally, and things get even more complicated. How, exactly, now, do we try to enforce emissions standards and living wages. Many efforts to rectify the issue would require giving conglomerating power, which makes them dubious strategies for a problem caused by high concentrations of power.

Big Names in Economics (And Big Feuds)

Read this section if: A) you have already read through Elle Magazine’s 65 page article on everyone who Taylor Swift is feuding/has feuded with and you are looking for a new source of drama (that page count is including ads, but still), B) you, like me, didn’t even have time to get through the list of female artists she’s feuded with but still need a celebrity feud fix, or C) aren’t reading an economics blog because of the celebrity gossip and are just interested in the ideas(I mean, if you say so).

Amazon vs. Walmart

Okay, so I initially was going to write this section only about theorists and philosophers, but I really do live for the drama and the billion dollar cat-fights. When Amazon announced that it was accepting bids, a business group in Little Rock, Arkansas (proud home of Walmart) made a video and took out an ad in the Washington Post, which is owned by Amazon’s CEO, to say that they didn’t want to deal with the traffic problems Amazon would cause. The ad reads like a break up letter from that one ex you have who really thought they were hiding the fact that they thought they were better than you. These, my friends, are the lifestyles of the rich and famous. One day we too can aspire to have the money to be petty in such an expensive manner. (To be clear, I would absolutely high five the people who did this; I never said petty was always bad).

Rawls and Nozick

John Rawls and Robert Nozick pretty much go hand in hand in the cannon of political philosophy; the opening line of an encyclopedia entry on Nozick is as follows: “A thinker with wide-ranging interests, Robert Nozick was one of the most important and influential political philosophers, along with John Rawls, in the Anglo-American analytic tradition.” Of course, by hand in hand I mean they went to totally opposite ends of the spectrum. Interestingly, Rawls is mentioned in the second sentence of a different encyclopedia entry on Nozick as well, but Nozick is barely a footnote in both entries on Rawls. Nozick’s name pops up as a critic or a counterpart to Rawls’ work exclusively.

Nozick is best known for his theory of Anarchy, State, and Utopia, and his theory centers around the principle that all people have a right to self-ownership. A person’s rights must be respected above all else, particularly the rights to life, liberty, and the fruits of one’s labor. His argument then is that state intervention is an infringement of rights, in particular redistributive taxation amounts to forcing labor by taking away part of the fruits. He doesn’t advocate for total anarchy, but instead a “night watchman” state, which forms essentially to perform only the regulatory needs that allow for the protection of rights (i.e. police).

Rawls on the other hand, has an utterly opposite principle, that a society should be structured in such a way that rather than prioritizing rights above all else, it prioritizes having the highest possible utility for the least well off of society, even if that means less overall social welfare.

Three key factors make up his argument, his principles of Justice as Fairness and the concept of the veil of ignorance, which is something of a thought experiment.

The principles of justice are described as follows by the Stanford Encyclopedia of Philosophy:

“First Principle: Each person has the same indefeasible claim to a fully adequate scheme of equal basic liberties, which scheme is compatible with the same scheme of liberties for all;

Second Principle: Social and economic inequalities are to satisfy two conditions:

They are to be to the greatest benefit of the least-advantaged members of society (the difference principle). (JF, 42–43)”

The veil of ignorance essentially says that we should strive for the society that we would want if we had no idea what position we would be born into (race, class, gender, nation, etc). In that way, we would want to make sure that even the lowest possible outcome is still a good option.

The two theories are totally mutually exclusive, as the “difference principle” mentioned in the encyclopedia entry demands income distribution, and focuses on society as a whole, while the Nozick model is totally driven by the welfare of the individual. That said, interestingly, both hold an ideal, be it fairness or selfhood, above optimizing social surplus. When we think of how many economic models focus on efficiency, thinking about, whether or not you agree with either of these two in the slightest, what else we might prioritize is important.

I also want to take a more serious note on the whole feuding aspect of these two to think about what it tells us about partisanship. These two have deep-rooted, fundamental beliefs that utterly oppose one another. When we look at the state of politics right now, I have no idea how to deal with the amount of partisanship we have (talk about inefficiency). I think, maybe, we have to start with figuring out what universal priorities we hold as a nation. I have to believe we have some, because otherwise we would all be hopeless. I also think looking at these two is a lesson in choosing your battles. Sometimes when we argue about politics, with family, on the internet, wherever it may be, it is an issue of someone being categorically, factually wrong. Sometimes, though, we just have to accept the fact that other people are fundamentally different from us and maybe consider the fact that they may not be totally awful because of it. Okay, I think that speech sufficiently balanced out the fact that I took so much joy in pettiness, so I’ll leave off there.

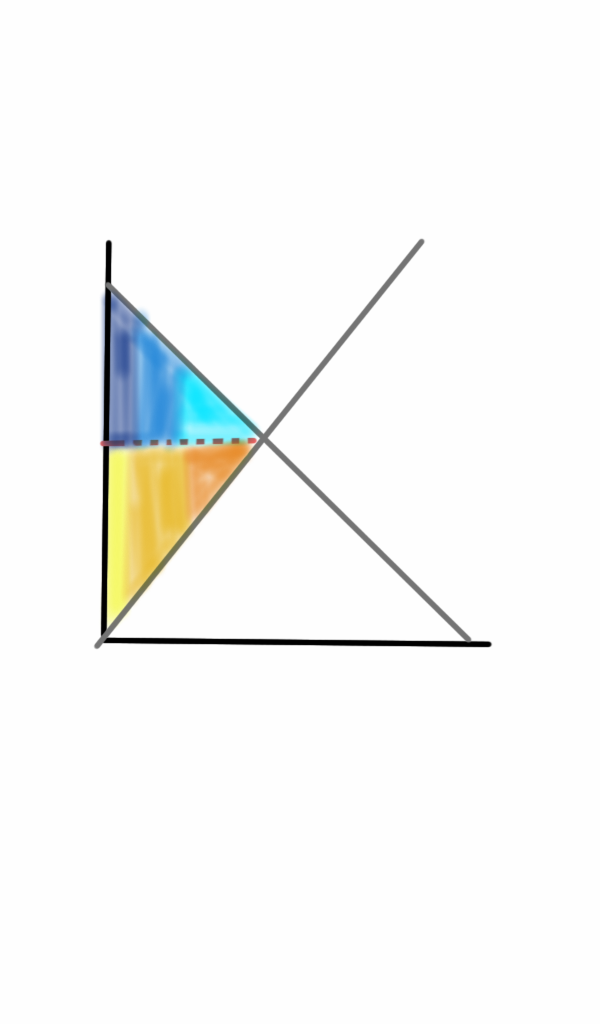

In economics 101, you learn about consumer surplus, producer surplus, and social surplus. For those of you unfamiliar with the concept, you can think about it in terms of when you go shopping and you see something you know you shouldn’t buy and you tell yourself “Okay if it’s less than X dollars, I’ll get it, but if not, I won’t.” That X, be it $5 or $50, is, in economic terms, your marginal benefit. Essentially, by setting that price point for yourself, you are implicitly saying that you think you will get X dollars worth of benefit from that good or service. The “marginal” comes in, because it is your benefit on the margin. So the benefit you get from owning one additional unit of that good or service. A demand curve plots the marginal benefit for different units. That is a slightly less concrete concept, because, for any given specific good, you usually get a certain amount of marginal benefit from buying it, and then you get no additional marginal benefit, or at least very little, from owning say two identical t-shirts or two copies of the same video game. But, you can think of it in a lot of different ways. First of all, you can think of it as a more aggregate concept. You get a lot of benefit from your first video game, and then another one gives you some additional benefit because you like variety, but not quite as much as the first game because the first game is the difference between having something to play and nothing to play at all; for clothing, even though our price point for shirts might depend on the specific shirt, in general you can aggregate them and think of how much you’re willing to spend on a first shirt as how much benefit you get from not having to go topless and each additional shirt as how much benefit you get from an extra day putting off doing laundry. That is just for your personal demand curve. The market demand curve, which is the sum of all of the demand curves in the market, is essentially how many goods you will sell to the population at a particular price point.

On a tangential note, I gave a lecture yesterday and now I keep having the instinct to add in “does that make sense?” which would, of course, make no sense to do (see what I did there?). But this seems like a good time to tell you that if you ever don’t understand what I’m saying, feel free to leave a comment!

Anyway, that’s demand, or marginal benefit. Supply is marginal cost, or how much it costs to produce an additional unit. You can think of that like when you are haggling with someone and you reach the lowest possible price that they were willing to sell for. So, if you say that you would have spent $X on something (lets say 10), and it turns out to cost $8, then you are paying $8 dollars on $10 worth of benefits. Look at you champ! You just got two dollars of consumer surplus!

If you buy something at a street fair for $10 because the person at the booth had that no-nonsense-not-a-chance-I-haggle face, but they totally would have sold it to you for $8, they have now gained $2 of producer surplus, and the personal satisfaction of thinking “suckerrrr” as you walk away.

If you look at the chart below, if the good is priced at equilibrium, social surplus (or the sum of producer and consumer surplus) is maximized.

The consumer surplus is the sum of the difference between the price and all of the buyers in the dark blue section, which is what they would have paid minus the equilibrium price, plus the slightly smaller medium blue section, plus the even smaller surplus for those in the light blue section, who would only be willing to pay a slightly higher price than the current price point. The surplus of each individual buyer makes up the consumer surplus total, and is represented by the area under the demand curve up until the price point, or the triangle formed between the price point, the quantity, and the Y intercept of the demand curve. Producer surplus works in the same way. The group of suppliers in yellow would be willing to sell for a lower price so they get the surplus between that price and the equilibrium price, and so on and so forth. Producer surplus is the area above the supply curve up until the price point, or the triangle formed by the price, the quantity, and the Y intercept of the supply curve.

When a monopoly sets their price at the profit maximizing point, as you can see, the producer surplus increases drastically while the consumer surplus becomes itty bitty.

The gray area you see is deadweight loss. A certain number of goods are being sold at a certain price point. If the price point were lower, more goods would be sold, and the surplus created by that would be greater than the surplus created by the monopoly situation. The surplus that we do not get is known as deadweight loss, and is represented by the gray area. Even though social surplus has shrunk, producer surplus has increased; the monopoly price maximizes producer surplus at the expense of consumer and overall surplus. This is known as allocative inefficiency.

Getting money is supposed to be the hard part, right. I mean, pulling a bank job takes hard work (and just working hard in general, I suppose, is no cake walk). So why does it have to be so complicated once you have it? (If you are seeking an answer to that question, please redirect your attention to the heavens and take a moment to raise your fist to the sky and rail at the universe; if you are seeking instead to try to understand what those complications are, read on.)

Inflation

Inflation is sort of like fat: you need some healthy fats in your diet to function, but if you have too much you’re in trouble. Rising prices are useful for a number of reasons. First of all, wages are sticky downwards. If a company needs to lower wages, they can do so by raising wage less than the rate of inflation, without lowering the nominal wage. Inflation also keeps the market moving: sitting with a huge pile of money under your mattress is less attractive when the money is losing value, and you would rather buy things now than when the price spikes. Bank or bond interest rates are also less attractive because high rates of inflation make real interest rates lower, which means less saving through those means as well.

Inflation also has a twin, deflation, which can have significantly worse consequences. If people think money is going to grow in value, they will put off spending it as long as possible. Think about if every single thing in the economy was always one day away from a clearance sale (yes, it is the things we love that have the power to hurt us most). You would never buy anything. And if no one is buying, then companies need to lay people off because they are not making money. And if people are unemployed and everything is about to go on clearance, you had better believe that they will be spending even less to try to make a finite supply last as long as possible. Meanwhile, companies won’t invest, because they won’t want to borrow, and without investment the cycle will just get worse. So, even without the positive effects, inflation is at least a way to stave off deflation.

That being said, we can have too much of a good thing (again, like clearance sales). One major issue is when inflation is felt unevenly throughout the economy. For instance, federal minimum wage has not changed in 11 years. The inflation chart from the bureau of labor statistics gives the inflation for the past 10; essentially, that means that the real minimum wage has decreased. Additionally, inflation rates are something that we calculate based on observable changes in the market, and our calculation system is by no means perfectly all encompassing. If price changes don’t affect every industry evenly, then people in certain industries are facing the same nominal income—that is to say, a lower real income, while others are getting that same real income (i.e. a higher nominal income, because of higher nominal sales, adjusted by the higher nominal cost of purchases). In the same vein, incomes are also redistributed from wage earners to profit earners, causing slower rise in wages.

Capital Gains Taxes

Capital Gains are taxed nominally, so inflation can lead to a decrease in real after tax income. Using a nominal measuring system, the IRS implicitly assumes that any price change on an asset reflects a change in the real value. Sometimes, it does (at least in part); often, it doesn’t. Resistance to higher rates of inflation largely stems from the fact that even if the inflation is controlled and expected, capital owners have to pay higher taxes without any change to their real wealth. If capital gains taxes were leveled against inflation adjusted value, then the tax would only be levied on the actual increase.

Neither a saver nor a lender be